I've been investing since the age of nine (two years earlier than Buffett), and like many investors, when I started out, my main goal was to become rich. When I started out (during the tech bubble), many investors had "champagne wishes and caviar dreams" and extremely unrealistic expectations.

In fact, I remember planning on doubling my money every year and asking my mother "what will I do with my trillions?!" The tech crash of 2000-2003 taught me the critical lesson that stock prices (

SPY) (

DIA) (

QQQ) don't grow to the sky, and that valuations (and fundamentals) always matter.

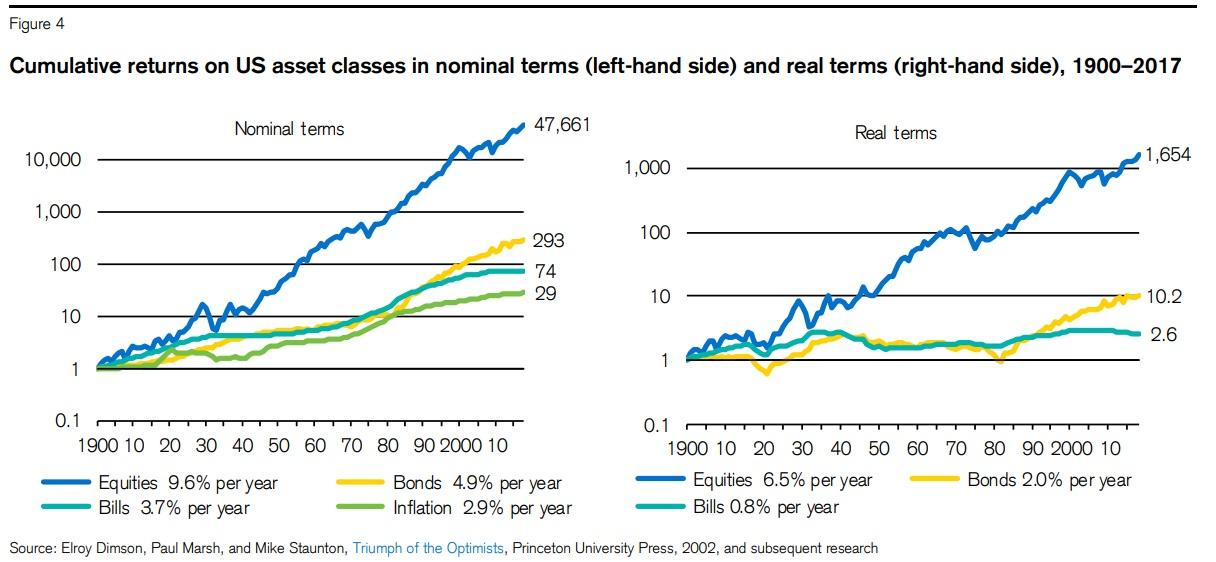

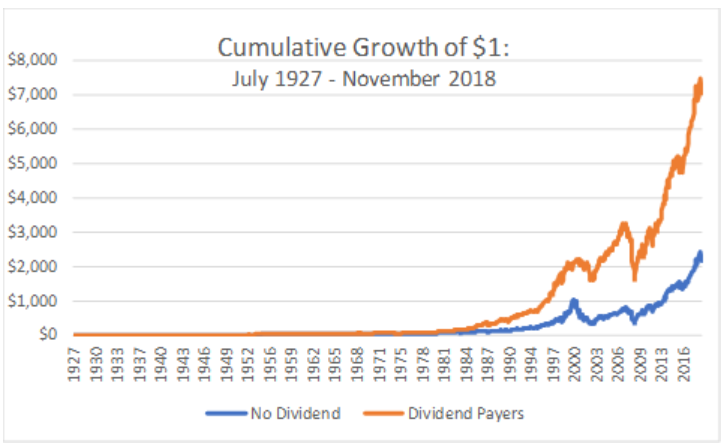

(Source: Credit Suisse Global Returns Yearbook 2018)

Despite the occasional bear market, stocks have indeed historically been the best way to exponentially grow wealth over time. But the sad truth is that most investors do very poorly at harnessing the awesome wealth-building power of the market.

Over the past two decades, the average retail investor hasn't benefitted from solid market returns, but has managed to underperform pretty much every asset class, and barely stay ahead of historically low inflation.

The goal I have with my writing isn't just in pointing out great, long-term investing ideas that can help you reach your financial goals, but more importantly to also teach you how to invest better.

And when it comes to the ultimate goal of most investors, to achieve financial freedom, my 23 years of experience, not to mention almost half a decade as a professional analyst and scholar of the investing arts, has taught me that three things are essential to achieving that dream I started out with at the tender age of nine.

In fact, without these three things, becoming (and staying) wealthy is virtually impossible. But more importantly, if you can master them, then financial independence is actually far easier than you think, and something you can probably achieve.

1. Live A Lifestyle Where Becoming "Rich" Is Easy

Morgan Housel is one of my favorite authors, and I consider him to be one of the wisest people on earth (on par with Buffett). Mr. Housel recently penned

a brilliant article that was actually the inspiration for this commentary.

The gist of that piece was that frugality, not blockbuster returns, is the most powerful way to achieve financial freedom.

"Personal savings and frugality - finance's conservation and efficiency - are parts of the money equation that are largely in your control and have a 100% chance at being as effective in the future as they are today... If we have the same assets and I can earn an 8% annual returns, and you can earn 12% annual returns, but I need half as much money to be happy while your lifestyle compounds as fast as your assets, I'm better off than you are. I'm getting more benefit from my investments despite lower returns." - Morgan Housel (emphasis added)

The most important point Housel makes, and that I agree 100% with, is that "rich" is subjective, and based on your expectations and choice of lifestyle. As Chris Rock famously said, "If Bill Gates woke up with Oprah's money he'd jump out the window."

Or to put it more eloquently, Jack Bogle, founder of Vanguard (and who recently passed away) liked to recount a famous story about author Kurt Vonnegut. At a party held by a hedge fund manager, Mr. Vonnegut's friend told him that their host had made more in a single day than his most famous novel, Catch-22, had made since it was published. To which Vonnegut replied, "Yes, but I have something he will never have...enough."

This is something I've learned the hard way, from years of living in poverty. My poor choice of spouse meant that several years ago my household expenses were far above our relatively strong income (about double the US median household's $60K per year).

My wife's family believed that money should be spent as fast as it was earned because "you could be hit by a bus tomorrow". They were trapped on the "hedonistic treadmill" in which trying to impress friends and family with materialistic one-upmanship was the order of the day, every day of the year.

Thus we lived in a nice house (bigger than we needed), filled with expensive furniture we rarely used, clothes we never wore, and our garage housed a BMW and Volvo SUV. We ate out twice a week, went to the movies frequently (and bought the overpriced concessions), and our savings rate was actually negative.

We lived beyond our means because my wife thought that was the key to happiness (and I foolishly refused to put my foot down over this profligate spending). But guess what? A never-ending and growing pile of debt, and the financial worries that go with it, more than offset any joys we got from fancy cars and expensive restaurant meals.

When job losses struck, our standard of living collapsed, and I literally spent several months starving, sometimes in the dark (our utilities were turned off several times). While I've managed to dig myself out of that financial hole since my divorce, I've never forgotten the most important lessons from those dark days (I call them my five years of financial tribulation).

Financial necessity forced me to live like a monk, and I learned that family, friends, dogs, and Netflix are all that you need to truly live a rich and fulfilling life.

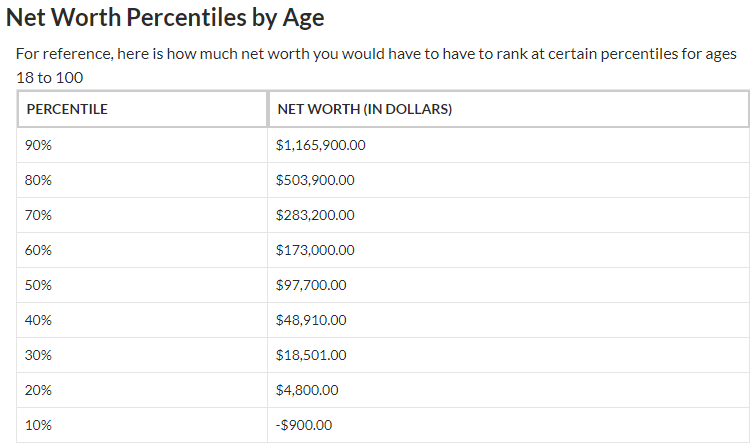

How does this apply to most people? Simply that "being rich" is not important, but rather "feeling rich" is. Here's a good example. I'm proud to say that within three years of my divorce, my net worth has gone from -$50,000 to $200,000.

If I were to compare myself to the entirety of the US population, then my $200K net worth puts me in the top 37% of Americans. While that's pretty good, for someone as competitive as me that could lead to discontent and unhappiness and a desire to drive that figure higher, like to $1.2 million to crack the top 10%.

But fortunately, my life experiences have taught me that happiness isn't about material things that money can buy, but the financial freedom it provides (to live how you want and on your own terms). What's more my career as an investment analyst and writer has taught me the importance of perspective.

For example, that same $200K net worth might only make me modestly well off compared to all Americans, but compared to 32-year-olds, I'm in the top 15.5%.

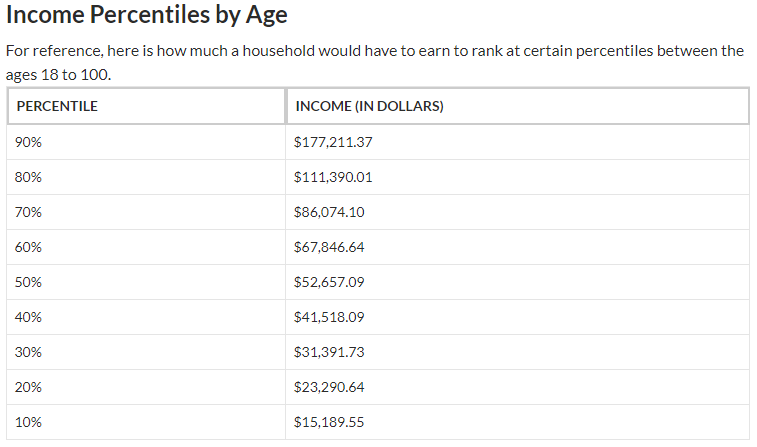

What's more my income last year ($173,000 from six different sources) puts me in the top 10.4% of Americans.

(Source: Shnugi.com)

Thanks to my frugal lifestyle, which I learned to love during those same terrible financial years in Alabama, my post-tax savings rate of 95% means that I'm assured to grow my net worth very quickly over time.

But I'm not here to brag about my success, but to point out that even the typical American needs to keep their financial position in perspective. For instance, the median US income in 2017 was

$31,786 and the median net worth of Americans today is $97,700.

Few would describe either the median US income or net worth as "wealthy" or "rich". But by global standards? According to globalrichlist.com, the median US income of just under $32,000 per year would mean you are:

- In the top 1.05% of global income earners, and

- the 63,036,801st richest person on earth in terms of income.

The US median income amounts to $16.56 per hour, which doesn't sound like much. It's soon going to be less than the starting wage at Target (

TGT) and Amazon (

AMZN). But here's what that modest wage amounts to globally:

- It's 207 times larger the average hourly wage in Ghana ($0.08/hr),

- 31 times the average annual income of workers in Zimbabwe,

- 60 times more than the average Indonesian worker makes, and

- it's 138 times more than the average Kyrgyzstani doctor makes.

And what about the "pitiful" $97,700 in net worth the average American has? Well, here's how it compares to the entire world:

- It puts you in the top 8.29% of people globally,

- it makes you the 373,121,207th richest person on earth,

- is enough to feed 100 Ethiopian families for a year, and

- is 70 times greater than the average wealth of someone in Myanmar.

When you think of your personal finances from a global perspective, then it's not hard to feel rich. Here's how I compare globally:

- I'm in the top 5.11% of people by net worth (the 230,012,296th richest person on earth and could feed 300 Ethiopian families for a year), and

- I'm in the top 0.05% of income earners (the 3,022,912th richest person in the world by income).

If you shift your perspective and, more importantly remember the whole point of making money is to put it to good use (not spend it on stupid stuff), then you're well on your way to achieving financial freedom and enduring happiness.

But there are two other vitally important things you have to do first to reach that goal, which ultimately is what we're all after.

2. Pick Long-Term Strategies With The Best Odds Of Success And Then Stick With Them

When I started investing at the peak of the dot-com bubble, it seemed like doubling your money each year was not just easy, but something even a blind monkey throwing darts at a newspaper could achieve.

(Source: Ploutos Research)

If only I had known then what I know now, I'd be a multi-millionaire. That's because while 100% annual returns are crazy (you'd multiply your money 1 billion fold every 30 years), stocks in general, and dividend growth stocks in particular, are indeed a way to grow your money by staggering sums over time.

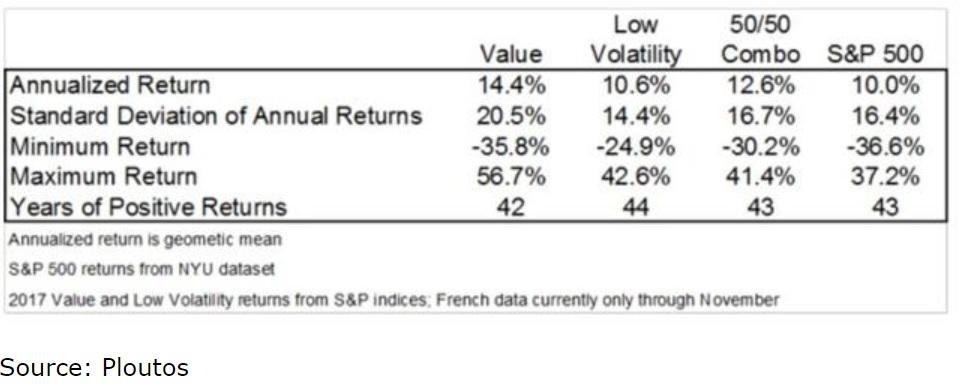

Stock Returns By Yield Quintile

(Source: Ploutos Research)

Now it's important to point out that while a fat yield is nice to have (and tends to outperform the market), quality must always come first. Ploutos, one of my favorite Seeking Alpha contributors, has crunched the numbers and found that the 10% highest-yielding companies tend to

be the worst performing of the dividend growth stocks.

That's because if a stock's yield is too high, it's likely due to weak fundamentals, such as a deteriorating business model in secular decline, horrible management, and a weak balance sheet. In other words, knowing the difference between a yield trap and a good high-yield company (whose fundamentals are strong) is critical. This is what I devote 70 hours per week to studying.

But while dividend growth investing is my personal favorite investing strategy, that doesn't mean it's the only road to riches.

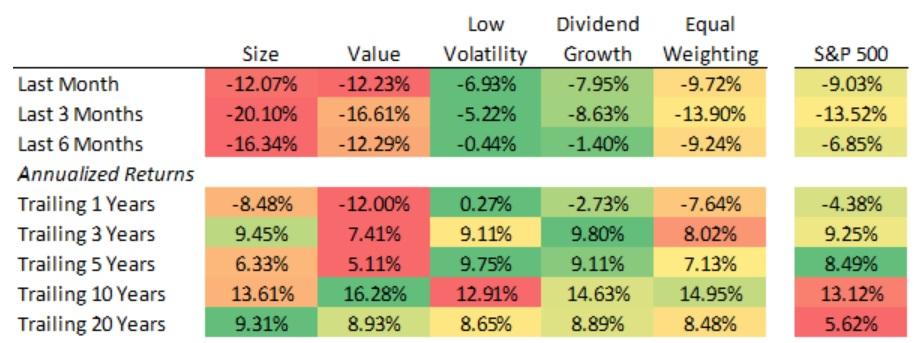

Returns By Investing Strategy

(Source: Ploutos Research)

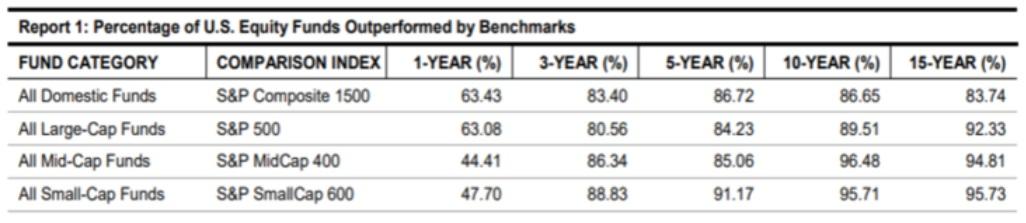

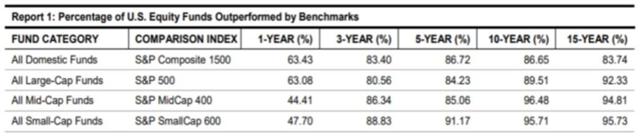

There are several strategies that have beaten the S&P 500 by a large amount for 20 years. That's pretty impressive given that less than 7% of Wall Street fund managers can even match the S&P 500 over a 15-year period.

(Source: S&P Global)

(Source: S&P Global)

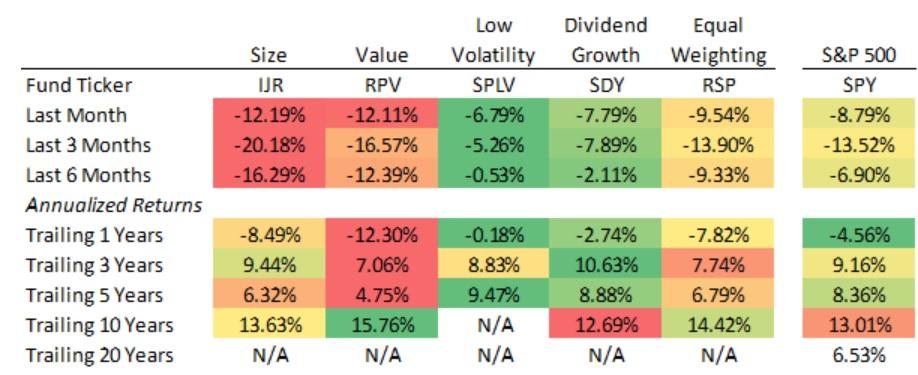

And note that these alpha factor strategies even have their own index funds in case you want to take a passive investing approach based on ETFs.

Alpha Factor ETF Returns

(Source: Ploutos Research)

The most important thing to remember, no matter what strategy you use, is that you need to be disciplined and patient. The greatest strategy in the world won't mean a darn thing if you have a zero or negative savings rate, and no strategy will outperform all of the time. Nor will any avoid down years or big crashes.

From 1926 to 2017, a 91-year period, low volatility and value stocks, two of the most successful strategies ever discovered, still had many down years, including some with very painful drawdowns.

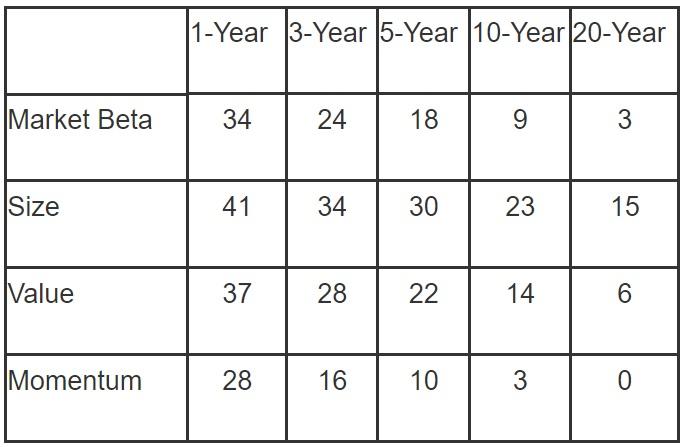

Probability Of Alpha Strategy Underperforming Market Over Rolling Time Periods

(Source: Advisor Perspectives)

What's more, any investing strategy, even if it does extremely well over time, will go through periods sometimes lasting decades where it underperforms.

This is where diversification comes in handy. I personally build my portfolios using several alpha factors, not just dividends, but also value, low volatility, and small caps. I also own several fast dividend growers, in numerous sectors, to ensure that I don't become mired in a frustrating and long period of underperformance that might shake my confidence and cause me to lose my discipline.

After all, the greatest investor in history, Warren Buffett (26% CAGR returns over his career) considers discipline to be his single greatest advantage.

Part of that discipline is patience because owning stocks means owning parts of a real company. You need to know why you bought it in the first place (the investment thesis) and not sell unless that thesis breaks, which seldom occurs in one quarter or even an entire year. Thus patiently waiting for your companies to execute on the long-term growth plans is one of the most important things great investors do.

But having realistic personal wealth goals, a frugal lifestyle, and the discipline to patiently execute over the long-term on the right combination of investing strategies is just how regular people can build wealth. In order to truly achieve financial freedom, you need one more thing, and it's the most important skill of all.

3. It's Not What You Make, But What You Keep That Counts

Meb Faber, the co-founder and the Chief Investment Officer of Cambria Investment Management, recently wrote

a great article that highlights the importance of not just building wealth but also keeping it.

Mr. Faber illustrated the need for a diversified portfolio that uses the right asset allocation for your needs with the example of Brazilian billionaire Eike Batista. Batista was hailed as a financial genius when, in 2012, his net worth hit $35 billion and he was the

7th richest person on earth.

But that business empire was so concentrated in oil and raw material exports and used so much leverage that when commodities crashed in 2014 Batista's fortune crashed with it, from $35 billion to -$1.2 billion. By 2017, he had managed to bring that up to $100 million...but got to enjoy that still substantial fortune while

in prison for various crimes including bribery and corruption of Brazilian (and other foreign) officials.

As Faber points out, Batista is merely the most extreme example (the first negative billionaire) of something that many rich families face, the loss of once impressive fortunes.

"Research has shown that 70% of wealthy families lose their wealth by the 2nd generation, and a whopping 90% by the third generation. Granted, some of that is due to high spending, addiction, bad luck, leverage, or just poor decisions. But a lot of it is how people invest their money." - Meb Faber (emphasis added)

According to Mr. Feber, the big mistake many investors make is improper asset allocation. That means their mix of stocks/bonds/cash and other asset classes is improperly structured. So in a bad year, it can result in such frightening losses, they panic, sell near the bottom and lock in large paper losses unnecessarily.

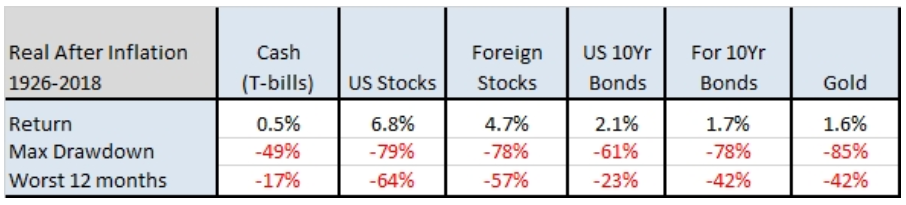

Inflation-Adjusted Total Returns By Asset Class

(Source: Cambria Investment Management)

As his table points out, there is NO asset class in the world that doesn't experience bear markets. Even "risk-free" US Treasuries have managed to lose 61% in inflation-adjusted terms during their worst stretch. And those same risk-free Treasuries have declined as much as 23% in a single year. Mind you that's nothing compared to the bloodbath stocks suffered during the Great Depression or the 85% decline that gold experienced at one point over a multi-year crash.

The point is that while frugality and a disciplined approach to the best investing strategies for your needs/risk profile/temperament is essential to becoming wealthy, asset allocation is the way you stay wealthy.

Unfortunately, the right asset allocation is different for everyone, based on your personality, goals, time horizon, income, savings rate, and a plethora of other factors. What's more, it changes over time as your life's situation and those various factors change.

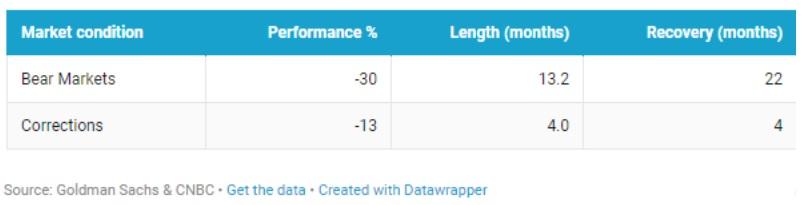

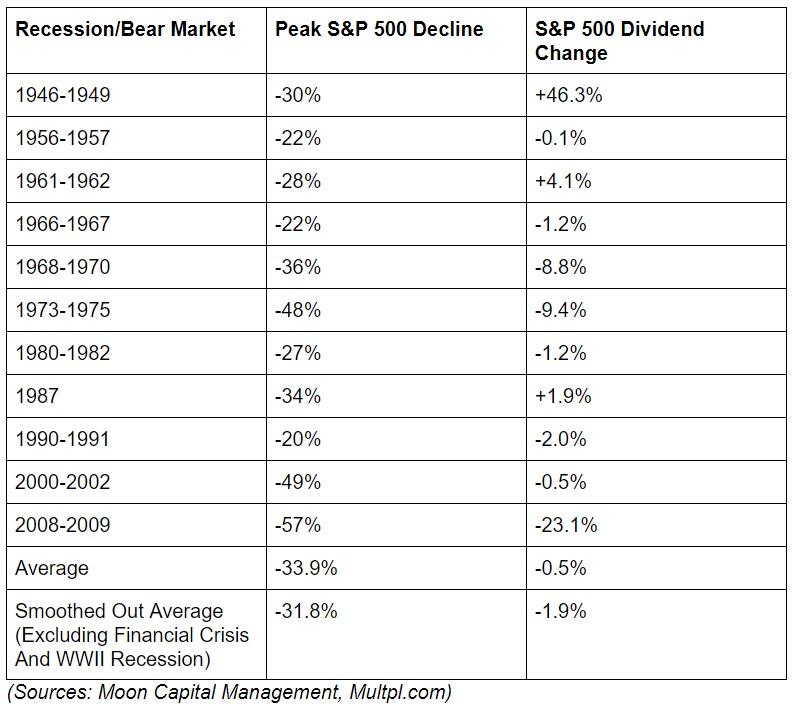

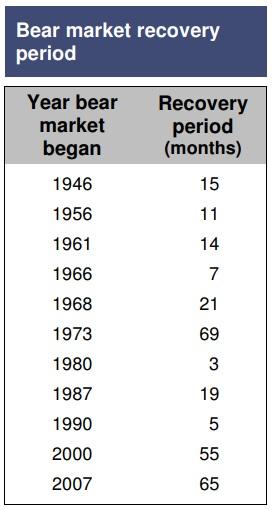

But a good rule of thumb is that a good asset allocation means having enough cash on hand to pay the bills (say during retirement) to avoid panic selling during a bear market in any particular asset. For stocks, the average bear market has lasted three years (since 1926) from market peak to new record highs.

(Source: Moon Capital Management)

(Source: Moon Capital Management)

But that's just the average. Stocks can sometimes take as long as six years to fully recover from an especially severe bear market. That's why you should try to plan for three years worth of cash to cover any needed expenses, but also own assets that are generally going up in a stock bear market (like bonds).

That allows you to avoid selling stocks, which appreciate the fastest over time, in order to pay the bills. Now, this is just a rule of thumb, and of course, your individual situation will vary.

Famed Seeking Alpha commenter Buy And Hold 2012 has been diligently saving and investing in dividend growth stocks since 1973. He's managed to invest about $500K so far, and his portfolio now pays him over $600,000 annually in exponentially growing dividends.

Does B&H 2012 need to worry about asset allocation? Should he have 10% of his portfolio in cash in case there's a bear market? Does he need to own bonds, or other non-stock assets to reduce his risk? In his case, he doesn't because his portfolio is nearly entirely (with a few exceptions) made up of low-risk blue-chip dividend growth stocks. These are companies that can be relied on to pay such an enormous amount of dividends each quarter that his standard of living will never be at risk no matter how much the market may crash, or how long it takes to recover.

That's because US companies are famous for not cutting dividends unless absolutely necessary and so a well-diversified blue-chip dividend portfolio can be expected to result in very stable and even growing income, even during a recession.

I personally plan to follow B&H 2012's example and stick to a 100% equity portfolio myself. But that's only because my personal situation is unusual. My high income, very high savings rate, and young age, mean that one day my dividend portfolio will be churning out such generous, safe, and fast-growing income that no matter how much the market might crash my standard of living (which will always be far more frugal than I can afford) will never be at risk. In fact, the excess dividends will be put to great use in a protracted bear market, so my long-term dividend income will only benefit from a long and painful market crash.

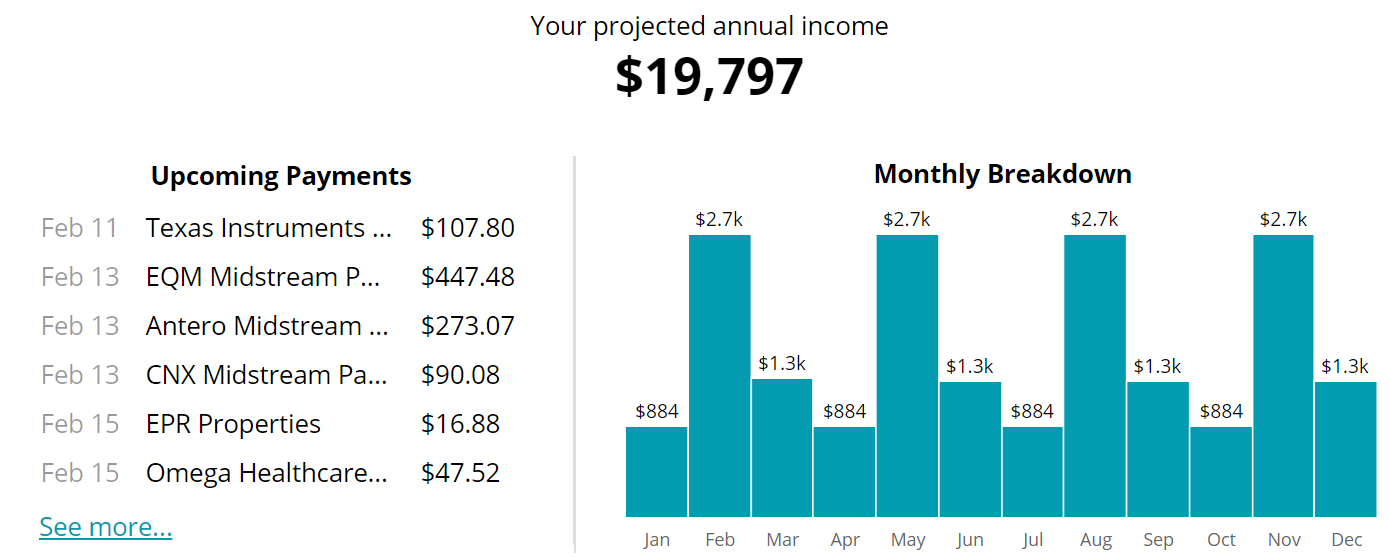

(Source: Simply Safe Dividends)

Heck, my retirement portfolio's current dividend stream is nearly $20K per year, which is enough for me to live on today, if I wanted to quit working forever. Factor in my portfolio's fast dividend growth rate and I would never have to invest another dollar again, and so could retire today if I didn't love what I do so much.

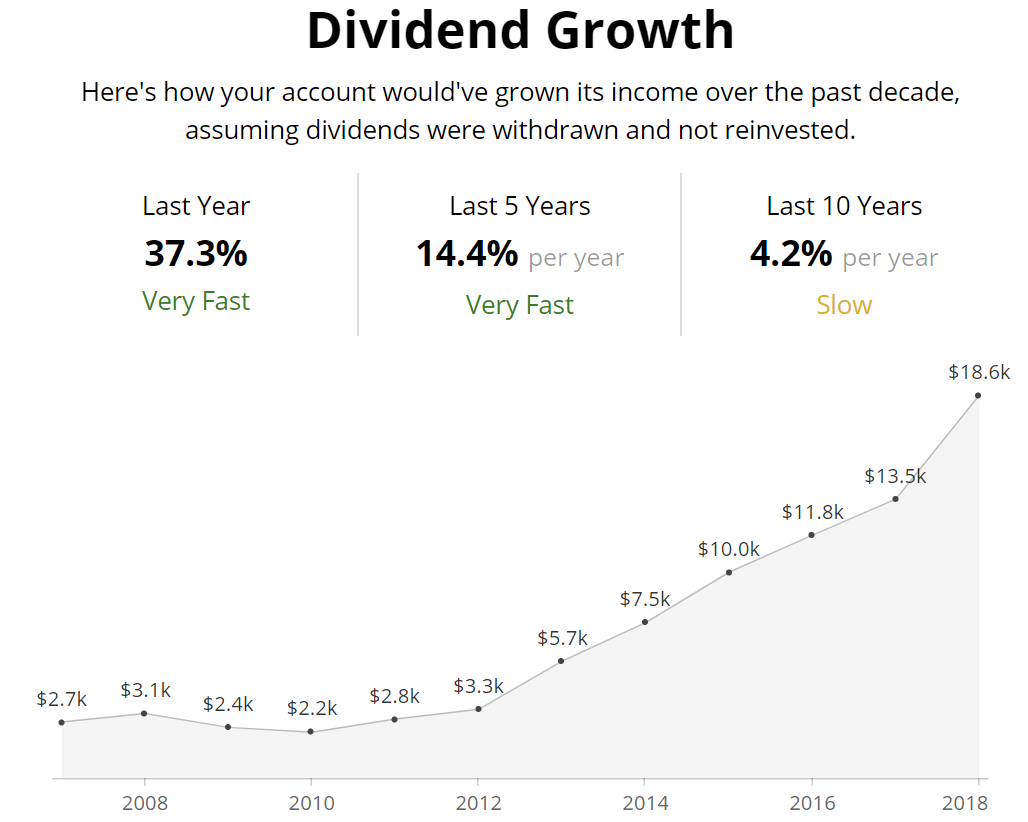

(Source: Simply Safe Dividends) - Note 5 Year forward dividend growth (according to Morningstar) is expected to be 13.9%

As to what you should do? Consult a certified financial planner (a fee-only fiduciary) to figure out the right asset allocation for your individual needs, and remember that you'll have to update your investing plan every few years because your risk profile will change over time.

Bottom Line: Achieving Financial Freedom Is Easy...If You Have The Right Mindset And Plan

For 23 years I, like many investors, have struggled to "crack the code" of the markets in a quest to become wealthy and financially independent. Along the way, I've learned what works, and more importantly, through the loss of several fortunes, what doesn't.

Over five years of transforming my greatest passion into my career, I've had the opportunity to study market history, behavioral economics, and the time tested strategies of the greatest investors of all time. And while the truth is that good investing (and good living) requires life-long learning, here's what I've learned is most critical to achieving the dreams investors have of achieving financial freedom.

First, you need to remember that being wealthy is about having income-producing assets, not spending lots of money. The guy driving the Bentley isn't necessarily richer (or happier) than you, but just has the income (and vanity) needed to support ludicrously massive car payments.

The truth is that a frugal lifestyle focused on the things that matter (friends, family, and self-actualization), rather than on consumption is one of the easiest ways to get "rich". Someone who can live comfortably and happily off a portfolio that's $300K in size doesn't need to have a sky-high income, massive savings rate, or go all in on the next Amazon.

That's good because while stocks can generate excellent returns over time, the truth is that the best long-term investment strategies for most people aren't based on hitting grand slams but merely lots of singles and doubles and avoiding striking out a lot.

That's why I've forever abandoned get quick rich strategies like short-term trading, option speculation and the use of dangerous amounts of leverage to boost my returns. Rather my focus is now entirely on quality, low-risk, undervalued dividend growth stocks, which is what I plan to recommend to most of my readers and invest my own money into going forward (

my Deep Value Dividend Growth Portfolio is beating the market by 8.4% so far).

While my strategy isn't necessarily right for everyone (there are lots of quality none dividend growth stocks you can buy), the reason I'm personally going with this approach is because of the most essential requirement for achieving financial freedom.

That would be the right asset allocation that's most likely to achieve your long-term goals. History is replete with investors who have made vast fortunes and then lost them even faster.

The most essential truth of investing, or life in general, is that money is merely a tool that must serve a higher purpose. For most of us, that means allowing us to spend as much of our lives doing what we want, with those we care about and maximizing our happiness.

While material things are necessary to some extent, it's easy to fall into the trap of thinking that more money will buy more happiness. Thus many investors take unnecessary risks with assets that have taken a lifetime to accumulate because they are trapped on the hedonistic treadmill in which your lifestyle grows along with your income and wealth over time.

Remember that the reason that getting rich over time works best is that the habits and discipline that allow you to become wealthy in the first place are the same habits that will keep you from going broke over time. The right asset allocation, which is different for everyone and ever-changing, is the best way to avoid the worst regret an investor can have, making a fortune and then losing it.

I have done that several times myself, and hope that articles like this can help others learn from my mistakes. The school of hard knocks has the most expensive tuition on earth and the best investing lessons are the ones you don't have to pay for yourself.

Disclosure: I am/we are long AMZN. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Dividend growth investing, master limited partnerships, REITs, long-term horizon