Thursday, May 31, 2018

Wednesday, May 30, 2018

Case Study 2

Case Study

Purpose

Here

is a scenario where our Fresh Start Program helped a family receive a 1

year mortgage at 4.99% and an improved cash flow of $2,700/month

- Client wants to consolidate all debts by refinancing their home, and have a fresh start by increasing their monthly cash flow

- 550 beacon due to 11 active trades that are at or near their limits

- Excellent mortgage repayment history

- GDS/TDS 39/42% with a stressed TDS of 48% using the mortgage rate plus 200 bps

- Client employed in full-time hourly position earning $100,000 per year verified by Employment Letter, verbal confirmation by employer, and T4

- Client receives $1,500 in Child Tax Credit income for their three children, verified by a Child Tax Receipt

- $780,000 appraised value

- Owner-occupied detached bungalow

- Good condition, well-maintained property

- Got offered a one year mortgage at 80% LTV to consolidate all their debts

- Additional $2,700 in monthly cash flow as monthly payments were lowered from $6,500 to $3,800

- MoneyValue will work with you to qualify you for the Fresh Start Program.

- Contact Me Today to see if you qualify.

T: 416 822 5886

e: edwin.m@moneyvalue.ca

Alternative Lending: Equityline Visa

ARE YOU SELF EMPLOYED WITH STATED INCOME, NON-TRADITIONAL INCOME?

The Home Trust Equityline® Visa.

The card that puts the equity in your home to work.

Financial flexibility that makes

your life easier.

Using the equity in your home can make life a lot easier. By securing your credit through a mortgage, you can open up a whole new world of financial flexibility:

Using the equity in your home can make life a lot easier. By securing your credit through a mortgage, you can open up a whole new world of financial flexibility:

Consolidate

high interest debts into one monthly payment

Renovate your home

Run your

business

Invest in your child’s education

Enjoy these great benefits with your Equityline Visa:

- No annual fee

- Interest paid only on the credit you use

- Visa Auto Rental Collision/Loss Damage Insurance

- Guaranteed hotel reservations

- The Visa Zero Liability Policy for protection against fraud

- Purchase Security Insurance, so you can shop at ease

- Automatic minimum deductions from your bank account, to avoid late payments

- Emergency card and cash replacement

- Convenient payment options using Pay Bills with Visa or your bank’s telephone and web banking services

- Access to cash at any ATM displaying the Visa or Plus logos, or by writing a convenience cheque

- Secure access 24/7 to your latest account information with Home Trust Visa Online

· Rates between 5.99% and 11.99% depending on

real estate collateral and borrower's credit

· Low monthly payments

· Earn

1% CashBack every time you make a purchase

Contact Me For More Information.

Edwin Masango

Tel: 416 822 5886

Email: edwin.m@moneyvalue.ca

Monday, May 28, 2018

Sunday, May 27, 2018

What Home Can you Buy in 2018?

The first steps in buying a house are ensuring you can afford to pay at least 5% of the purchase price of the home as a down payment and determining your budget.

This calculator steps you through the process of finding out how much you can borrow.

Friday, May 25, 2018

5 ways you can kill your mortgage approval

So, you found your dream home, negotiated a fair price which was

accepted. You supplied all the needed documentation to your mortgage

broker and you are waiting for the day that you go to the lawyer’s to

sign the final paperwork and pick up the keys.

All of a sudden your broker or the lawyer calls to say that there’s a problem. How could this be? Everything has been signed and conditions have been removed. What many home buyers do not realize is that your financing approval is based on the information the lender was provided at the time of the application. If there have been any changes to your financial situation, the lender is within their rights to cancel your mortgage approval. There are 5 things that can make home financing go sideways.

1 Employment – You were working for ABC company as a clerk for 5 years making $50,000 a year and just before home possession you change jobs. The lender will now ask for proof that probation for this new job is waived and new job letters and pay stubs at the very least. If you change industries they will want to see more proof that you are capable of keeping this job.

If your new job involves overtime or bonuses of any kind that vary over time, they will ask for a 2 year average which you will not be able to provide.

Another item that could ruin your chances of getting the mortgage is if you decide to change from an employee to a self-employed contractor just before possession day. Even though you are in the same industry, your employment status has changed . This is a big deal killer.

2. Debt – A week or two before your possession date, the lender will obtain a copy of your credit report and look for any changes to your debt load. Your approval was based on how much you owed on that particular date. Buying a new car or items for the new home need to be postponed until after possession of your new home.

Don’t be fooled by “Do not pay for 12 months” sales campaigns. You now owe this money regardless of when the payments start. Don’t buy a new car and don’t buy furniture for the new home. This will increase your debt ratio and can nullify your financing.

3. Down payment source – And yet again I reiterate that the approval is based on the initial information you have provided. You will be asked at the lawyer’s office to verify the source of the down payment and if it is different than what the lender has approved, then you may be in trouble. For example, you said that you were going to save the funds and then at the last minute Mom and Dad offer you the funds as a gift. There’s no problem accepting the gift if the lender knows about it in advance and has included this in their risk assessment, but it can end a deal.

4. Credit – Don’t forget to make your regular credit card payments. If your credit score falls due to late payments, this can kill your financing. If you have a high ratio mortgage in place which required CMHC insurance, a lower credit score could mean a withdrawal of their insurance once again , killing the deal.

5-Identity Documents – This can be a deal killer at the lawyer’s office. The lawyer is required to verify your identity documents and see that they match the mortgage documents. Many Canadians use their middle names if they have the same name as their parent. Lots of new Canadians adopt a more Canadian sounding name for their day-to-day lives but their passports and other documents show another name.

Be sure to use your legal name when you apply for a mortgage to avoid this catastrophe . Finally, keep in touch with your Mortgage professional right up to possession day. Make this a happy experience rather than a heartbreaking one.

David Cooke

All of a sudden your broker or the lawyer calls to say that there’s a problem. How could this be? Everything has been signed and conditions have been removed. What many home buyers do not realize is that your financing approval is based on the information the lender was provided at the time of the application. If there have been any changes to your financial situation, the lender is within their rights to cancel your mortgage approval. There are 5 things that can make home financing go sideways.

1 Employment – You were working for ABC company as a clerk for 5 years making $50,000 a year and just before home possession you change jobs. The lender will now ask for proof that probation for this new job is waived and new job letters and pay stubs at the very least. If you change industries they will want to see more proof that you are capable of keeping this job.

If your new job involves overtime or bonuses of any kind that vary over time, they will ask for a 2 year average which you will not be able to provide.

Another item that could ruin your chances of getting the mortgage is if you decide to change from an employee to a self-employed contractor just before possession day. Even though you are in the same industry, your employment status has changed . This is a big deal killer.

2. Debt – A week or two before your possession date, the lender will obtain a copy of your credit report and look for any changes to your debt load. Your approval was based on how much you owed on that particular date. Buying a new car or items for the new home need to be postponed until after possession of your new home.

Don’t be fooled by “Do not pay for 12 months” sales campaigns. You now owe this money regardless of when the payments start. Don’t buy a new car and don’t buy furniture for the new home. This will increase your debt ratio and can nullify your financing.

3. Down payment source – And yet again I reiterate that the approval is based on the initial information you have provided. You will be asked at the lawyer’s office to verify the source of the down payment and if it is different than what the lender has approved, then you may be in trouble. For example, you said that you were going to save the funds and then at the last minute Mom and Dad offer you the funds as a gift. There’s no problem accepting the gift if the lender knows about it in advance and has included this in their risk assessment, but it can end a deal.

4. Credit – Don’t forget to make your regular credit card payments. If your credit score falls due to late payments, this can kill your financing. If you have a high ratio mortgage in place which required CMHC insurance, a lower credit score could mean a withdrawal of their insurance once again , killing the deal.

5-Identity Documents – This can be a deal killer at the lawyer’s office. The lawyer is required to verify your identity documents and see that they match the mortgage documents. Many Canadians use their middle names if they have the same name as their parent. Lots of new Canadians adopt a more Canadian sounding name for their day-to-day lives but their passports and other documents show another name.

Be sure to use your legal name when you apply for a mortgage to avoid this catastrophe . Finally, keep in touch with your Mortgage professional right up to possession day. Make this a happy experience rather than a heartbreaking one.

David Cooke

Dominion Lending Centres - Accredited Mortgage Professional

Saturday, May 19, 2018

Thursday, May 17, 2018

Would you like to save money without worrying about taxes?

A Tax-Free Savings Account (TFSA) is an easy way to save and withdraw, without tax implications.

1. A TFSA is an easy way to save.

Contact Us To Open a TFSA Today

5 great reasons to open a TFSA with MoneyValue:

1. A TFSA is an easy way to save.

- A TFSA is designed for anyone aged 18 or older looking to save for a short-, medium- or long-term goal.

- A TFSA with MoneyValue gives you the option to place your savings in a Guaranteed Interest Account or a Segregated Fund, providing even more protection!

- Amounts deposited in a TFSA and the income generated (e.g. Investment income and capital gains) are tax sheltered, meaning no tax implications for your returns.

- The money you withdraw during one calendar year increases your TFSA contribution limit for the following year to the same amount you withdrew.

- The amount you save in a TFSA during any given year has no impact on the maximum amount you can contribute to an RRSP, which is based on your income.

- Caution: know your limit! If your annual contributions are over the limit, you will be taxed on the excess amount, which you will have to withdraw from your TFSA.

Contact Us To Open a TFSA Today

Wednesday, May 16, 2018

SECOND MORTGAGE

SECOND MORTGAGES up to 95% LTV for:

1. Debt Consolidation

2. Purchase Assist (Help with Down Payment)

3. Equity Takeout (Cash for whatever reason)

LENDING GUIDELINES:

-

up to 95% LTV*

-

Loan amount: $10,000 - $250,000

- Interest rate: Starting at 6.

99% - Income: Employed, Self

employed (Self-declared income welcome); - Credit: BEACON SCORE or RATIOS (TDS/GDS) are NOT CONSIDERED;

- CONTACT ME TODAY

- t: 416 822 5886

Private Lending Available

Private Lending Up To 85% LTV in the GTA!!!

1st and 2nd Residential Mortgages

Get your Spring into full gear! Let us help you with some of those tough deals now!

- Fast Turnaround on Applications; Decision within 24 hours

- Competitive Rates and "Fair Lender Fees"

- Rates starting at 10% for Seconds

- Common Sense Underwriting to make deals work for your clients

- No Minimum Beacon Score

- Quick Closings

- Funds Immediately Available

- Construction Loans

- APPLY TODAY

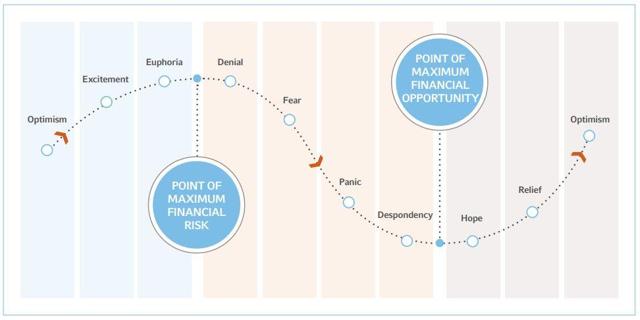

Hope is not an Investment Strategy!

I expect that most serious investors (meaning, my

readers) are well aware of market cycles. And often, how they feel about

the market also runs in cycles. This chart, “The Market Cycle of Emotions”, best illustrates and identifies how investors may be feeling during points of the market cycle.

(Source)

A

few weeks ago, I was reading comments on Seeking Alpha, and one of my

valued readers, RoseNose, said she was “hoping” for the best. As Richard

Russell wrote in one of his Dow Theory letters...

“Any time you find yourself hoping in this business, the odds are that you are on the wrong path - or that you did something stupid that should be corrected.”

“I have seen a lot of hopes ending in disasters simply because people made mistakes in buying bad businesses or expensive stocks, and then hoped that a tooth fairy would absolve them by taking the prices higher!...

“Unfortunate it may sound, but hope is a big money-loser in the investment business. It is hope that keeps you from selling your losing stocks. It is hope that stops you from cutting your losses before they get bigger. It is hope that leads you to buy good businesses at super-expensive prices.”

Khandelwal adds:

“But please... please don’t HOPE! Avoid it! Instead, embrace patience and reality... however painful it may be. And finally remember this - there are many good investing strategies: buying cheap stocks, buying high quality businesses, turnarounds, top down, bottom up, to name only a few. Hope is not among them.”

As a true “value investor”,

I’ve learned to take the emotion out of the investing process, and

instead, rely on data and reasoning. That’s not to say I don’t embrace

my “gut feelings” for a stock - after all, I minored in psychology (over

25 years ago), while majoring in business (at Presbyterian College).

However,

fundamental analysis is the best strategy for me, and it’s one that

allows me to take the guesswork out of the investing process. “Hope” is

not part of my vocabulary. As Benjamin Graham said:

“Most of the time common stocks are subject to irrational and excessive price fluctuations in both directions as the consequence of the ingrained tendency of most people to speculate or gamble... to give way to hope, fear and greed.”

My SWAN Strategy

Many of you on Seeking Alpha are aware of my SWAN strategy, and of course, the acronym that stands for “sleep well at night”.

I

certainly did not coin the term SWAN investing, but I am certainly a

disciple of the method of analyzing stocks using fundamental analysis.

After all, from a value investor’s perspective, “You are neither right

nor wrong because the crowd disagrees with you. You are right because

the data and reasoning are right.”

As far as I’m

concerned, SWAN investing boils down to minimizing risk, and every

investor should use his or her set of principles to form their own

philosophy. While it is impossible to eliminate all investment risk,

value investors can greatly minimize risk by filtering out the

disadvantageously positioned companies from the outset.

It’s

important to take the emotion out of investing and not rely on hope,

panic, or optimism to form an opinion. Value investors have the extra

security of knowing that they own quality stocks that have one or more

attributes of long-term winners.

That’s the primary

reason that my SWAN strategy has proven to be successful. While I wish I

could claim that my basket of SWANs have outperformed year to date, I

can say that my long- term success is rooted in selecting REITs with a

significant margin of safety.

In other words, if I do a

good job at screening the best SWANs, I am less concerned with the

behavioral aspect (i.e., hope, panic, etc.). In fact, I can use this to

my advantage - when I see fear overblown (i.e., rising rates and retail

apocalypse), I sharpen my pencil and scout for the very best SWANs,

recognizing that at some point “the storm will subside, and a sunnier

and more plentiful time is bound”.

Always remember,

the present price is based on a mix of unpredictable factors, many of

which pertain more to the market cycle of emotions, so it is virtually

impossible for anyone (even RoseNose) to predict future prices

accurately.

It’s the job of an Intelligent REIT

Investor to capitalize upon “a favorable difference between price on the

one hand and indicated or appraised value on the other”. When asked

what keeps most individual investors from succeeding, Benjamin Graham

had a concise answer:

“The primary cause of failure is that they pay too much attention to what the stock market is doing currently.”

Tuesday, May 15, 2018

THE BEST WAY TO RESEARCH A COMPANY FOR A JOB INTERVIEW

Before you go on a job interview, it’s important to find out as much

as you can about the company. That way you’ll be prepared both to answer

interview questions and to ask the interviewer questions. You will also

be able to find out whether the company and the company culture are

a good fit for you.

Take some time, in advance, to use the Internet to discover as much information as you can about the company.

Spend time, as well, tapping into your network to see who you know who can help give you an interview edge over the other candidates. Here’s how to research a company.

Start by visiting the company website. There, you can review the organization’s mission statement and history, products and services, and management, as well as information about the company culture. The information is usually available in the About Us section of the site. If there’s a Press section of the website, read through the featured links there.

Browse Social Media

Next, check the company’s social media accounts. Visit their Facebook, Google+, Instagram, and Twitter pages. This will give you a good sense of how the company wants its consumers to see it. Like or follow the company to get updates. You’ll find information you may not have found otherwise.

Use LinkedIn

LinkedIn company profiles are a good way to find, at a glance, more information on a company you’re interested in. You’ll be able see your connections at the company, new hires, promotions, jobs posted, related companies, and company statistics. If you have connections at the company, consider reaching out to them – not only can they put in a good word for you, but they may also share their perspective on the company and give you tips that will help you ace the interview.

As well, take a look at your interviewer’s LinkedIn profile to get insight into their job and their background.

Get an Interview Edge

Glassdoor’s Interview Questions and Reviews section has a goldmine of information for job seekers.

You can find out what candidates for the positions you are interviewing for were asked and get advice on how tough the interview was. Use reviews to help get a sense of company culture. That said, take them with a grain of salt – employees are often most likely to leave reviews when they are unhappy. As you read reviews, look for repeated themes. The more mentions a given subject gets (whether it’s praise for flexible hours or frustration with senior management) the more likely it is to be accurate.

Use Google and Google News

Search both Google and Google News for the company name. This can be really invaluable. You may find out that the company is expanding into Asia, for instance, or received a round of start-up funding. Or, you may find out that a recent product underperformed or had to be recalled. This knowledge can help shape your responses to interview questions.

Tap Your Connections

Do you know someone who works at the company? Ask them if they can help.

As well as researching the company, it makes sense to review the overall industry. If you’re interviewing for a job at a mortgage company, for instance, it’s helpful to be informed about current home ownership trends. Get to know the company’s biggest competitors and identify their successes and flaws, too. Insight into the company’s industry and rivals is bound to impress interviewers.

Take some time, in advance, to use the Internet to discover as much information as you can about the company.

Spend time, as well, tapping into your network to see who you know who can help give you an interview edge over the other candidates. Here’s how to research a company.

Tips for Researching Companies Before Job Interviews

Visit the Company WebsiteStart by visiting the company website. There, you can review the organization’s mission statement and history, products and services, and management, as well as information about the company culture. The information is usually available in the About Us section of the site. If there’s a Press section of the website, read through the featured links there.

Browse Social Media

Next, check the company’s social media accounts. Visit their Facebook, Google+, Instagram, and Twitter pages. This will give you a good sense of how the company wants its consumers to see it. Like or follow the company to get updates. You’ll find information you may not have found otherwise.

Use LinkedIn

LinkedIn company profiles are a good way to find, at a glance, more information on a company you’re interested in. You’ll be able see your connections at the company, new hires, promotions, jobs posted, related companies, and company statistics. If you have connections at the company, consider reaching out to them – not only can they put in a good word for you, but they may also share their perspective on the company and give you tips that will help you ace the interview.

As well, take a look at your interviewer’s LinkedIn profile to get insight into their job and their background.

Get an Interview Edge

Glassdoor’s Interview Questions and Reviews section has a goldmine of information for job seekers.

You can find out what candidates for the positions you are interviewing for were asked and get advice on how tough the interview was. Use reviews to help get a sense of company culture. That said, take them with a grain of salt – employees are often most likely to leave reviews when they are unhappy. As you read reviews, look for repeated themes. The more mentions a given subject gets (whether it’s praise for flexible hours or frustration with senior management) the more likely it is to be accurate.

Use Google and Google News

Search both Google and Google News for the company name. This can be really invaluable. You may find out that the company is expanding into Asia, for instance, or received a round of start-up funding. Or, you may find out that a recent product underperformed or had to be recalled. This knowledge can help shape your responses to interview questions.

Tap Your Connections

Do you know someone who works at the company? Ask them if they can help.

If you’re a college grad, ask your Career

Office if they can give you a list of alumni who work there. Then email,

send a LinkedIn message, or call and ask for assistance.

Get to Know the Industry and CompetitorsAs well as researching the company, it makes sense to review the overall industry. If you’re interviewing for a job at a mortgage company, for instance, it’s helpful to be informed about current home ownership trends. Get to know the company’s biggest competitors and identify their successes and flaws, too. Insight into the company’s industry and rivals is bound to impress interviewers.

How to Use This Research During Interviews

During a job interview, interviewers ask questions to get to know candidates. But their main goal is to determine if a candidate will be a good fit for the position and company.

Your company research will make your responses to

questions compelling and show that you’ll be helpful to their goals and

bottom line.

Plus, your knowledge will help you give a specific answer if you’re

asked why you’d like to work for the company. You can share details

about things you find admirable about the company, its mission, or its

culture.The Spring Housing Market Is Off To A Slow Start

April

is usually the start of a spring housing market ramp-up, but this year

the new mortgage stress test and rising mortgage rates have continued to

be a negative factor. Those expecting an early-stage pick-up marking an

end to the payback for sales pulled forward into the fourth quarter of

last year have been sorely disappointed.

Local real estate boards in Toronto and Vancouver announced that activity was weak in both markets in April--down just over 32% in Toronto and by 27.4% in Vancouver relative to a year ago. In Toronto, the weakness in April reflected at least in part a decline in new listings as would-be sellers might still find it hard to list at today's lower prices for single-family homes.

Local real estate boards in Toronto and Vancouver announced that activity was weak in both markets in April--down just over 32% in Toronto and by 27.4% in Vancouver relative to a year ago. In Toronto, the weakness in April reflected at least in part a decline in new listings as would-be sellers might still find it hard to list at today's lower prices for single-family homes.

Price-wise,

developments last month should please policy-makers. Toronto’s

aggregate benchmark price fell below year-ago levels (which constituted

all-time highs in the area) for the second-straight month by

5.2%—providing some much-needed affordability relief. Single-detached

prices (down 10.3% year-over-year) contrasted starkly with condo prices

(up 10.2%). On a year-over-year basis, the drop in the aggregate price

virtually matched the decline recorded during the 2008-09 recession.

The

annual rate of benchmark price increases in the Vancouver region has

slowed as well in the past two months. In April, that rate eased back

below 15% for the first time since November last year. The deceleration

isn’t doing much yet to improve affordability in the area, but it will

be considered a sign that the market might be changing course away from

overheating. The suite of market-cooling measures announced in the 2018

BC budget is poised to keep prices on this decelerating path over the

coming months.

On

a national basis, data released today by the Canadian Real Estate

Association (CREA) show a 2.9% decline in home sales from March to April

to the lowest level in more than five years (see chart below). About

60% of all local housing markets reported fewer sales, led by the Fraser

Valley, Calgary, Ottawa and Montreal.

|

|

|

Chief Economist, Dominion Lending Centres

drcooper@dominionlending.ca

Non-Partisan Investing: Financial Advisors' Daily Digest

In his weekly “Weighing the Week” column, Jeff Miller

presents evidence for continued economic expansion, of surprising

strength. He’s been saying so for some time, and deserves credit for

being right.

In contrast, I see a much larger volume

of articles talking about the doom and gloom soon to befall us. This

latter type of article falls into two categories: intelligent analyses

and pulp pessimism. While I too see, and write often, about the

long-term problems that I believe will bring about a day of reckoning,

if unaddressed, I take no position on when that might happen, and that

is why I advocate a portfolio that can benefit from the market’s

continuing strength while offering protection from market declines,

i.e., the sort of portfolio lacking appeal to “partisan” investors, for

whom bull or bear market scenarios are akin to party allegiance.

Jeff’s article

offers numerous reasons to be upbeat about the economy. For example,

here is just one snippet about stock buybacks (John M. Mason’s piece,

linked below, also discusses this issue):

Corporate buybacks are bullish for investors. (Barron’s cover story) Andrew Bary’s analysis is thorough, looking at many stocks and considering counter-arguments in an even-handed way. Buybacks add an effective ‘yield’ of about 3%, combined with a 1.9% dividend yield on the S&P 500.”

This is a perfect

example of a phenomenon that could be looked at very differently,

depending on your investment “party.” By buying back their own shares,

corporations reduce the number of shares outstanding and thereby cause

earnings per share to rise. That’s fantastic news for existing

shareholders! But here’s the catch: In order to buy back these shares,

the same companies are issuing large quantities of debt that will one

day have to be repaid; and – about those earnings per share: their rise

occurs irrespective of whether their actual profits rose!

So while I might write

pessimistically about corporate underinvestment in labor and capital

expenditure, or about the fact that managers looking after shareholders

via buybacks tend to be showered with bonuses and options, I acknowledge

that such a trend is apt to fuel stock prices, barring some large-scale

jolt.

Currently, however, the biggest large scale

jolt that I see presently (though perhaps not presciently – I could be

wrong) is peace breaking out. I quote the following marvelous snippet

from today’s Wall Street Breakfast:

"North Korea has announced that they will dismantle Nuclear Test Site this month, ahead of the big Summit Meeting on June 12th. Thank you, a very smart and gracious gesture!" President Trump wrote on Twitter. Pyongyang plans to destroy all of the tunnels at the country’s northeastern testing ground with an explosion and remove observation facilities, research posts and ground-based guard units.”

As I wrote last week,

commenting on Rob Marstrand’s bullish case for purchasing a South Korea

country ETF, North Korea’s peace moves appear to be legit, and if so,

would lift a boulder off of South Korea’s muscular shoulder; imagine

mighty South Korea unhindered by the shadow of North Korea’s nuclear

cloud.

As Jeff Miller asks in his article, the

question pundits should be asking themselves is what investments are

most apt to benefit from administration policy. He astutely adds that

“this is an investment question, not a political one.” For me, the

investment I’ll be weighing this week is whether and when to buy a South

Korea ETF.

TD Bank joins rival in discounting 5-year variable mortgage rate

TORONTO -- TD Bank is joining a rival bank in offering a highly

discounted variable mortgage rate as competition among Canada's biggest

lenders heats up.

The Toronto-based bank said Tuesday it's lowering its five-year variable closed rate to 2.45 per cent, or 1.15 per cent lower than its TD Mortgage Prime rate, until May 31.

TD's special rate follows last week's move by the Bank of Montreal, which discounted its variable mortgage rate to 2.45 per cent until the end of May.

Canada's lenders often offer special spring mortgage rates as homebuying activity picks up, but mortgage planner Robert McLister said last week that BMO's special discounted variable rate was the biggest widely advertised discount ever by a Big Six Canadian bank.

TD's discounted rate on Tuesday brings its variable mortgage rate offer in line with BMO's.

TD spokeswoman Julie Bellissimo says its special five-year variable rate applies to new and renewed mortgages, as well as the variable rate term portion of certain TD home equity lines of credit.

"We are confident this is a strong offer for new and renewing customers, while ensuring we remain competitive in a changing environment," Bellissimo said in an emailed statement.

The moves come amid slowing mortgage growth. The Canadian Real Estate Association said Tuesday that national home sales volume sank to the lowest level in more than five years in April, falling by 13.9 per cent from the same month last year. The national average sale price decreased by 11.3 per cent year-over-year.

Home sales have slowed due to various factors, including measures introduced the Ontario and B.C. governments to cool the housing market, such as taxes on non-resident buyers.

Other headwinds for mortgage growth include higher interest rates and a new financial stress test that makes it more difficult for would-be homebuyers to qualify with federally regulated lenders, such as the banks.

As of Jan. 1, buyers who don't need mortgage insurance must prove they can make payments at a qualifying rate of the greater of two percentage points higher than the contractual mortgage rate or the central bank's five-year benchmark rate. An existing stress test also stipulates that homebuyers with less than a 20 per cent down payment seeking an insured mortgage must qualify at the central bank's benchmark five-year mortgage rate.

The tighter lending rules are making it harder for homebuyers to qualify for uninsured mortgages, and shrinking the pool of qualified buyers for higher-priced homes, CREA's chief economist Gregory Klump said in April.

Meanwhile, Canada's largest lenders all raised their benchmark posted five-year fixed mortgage rates in recent weeks as government bond yields increased, signalling a rise in borrowing costs.

In turn, the central bank's five year benchmark qualifying rate -- which is calculated using the posted rates at the Big Six banks -- increased last week to 5.34 per cent. This qualifying rate is used in stress tests for both insured and uninsured mortgages, and an increase means that the bar is now even higher for borrowers to qualify.

The Toronto-based bank said Tuesday it's lowering its five-year variable closed rate to 2.45 per cent, or 1.15 per cent lower than its TD Mortgage Prime rate, until May 31.

TD's special rate follows last week's move by the Bank of Montreal, which discounted its variable mortgage rate to 2.45 per cent until the end of May.

Canada's lenders often offer special spring mortgage rates as homebuying activity picks up, but mortgage planner Robert McLister said last week that BMO's special discounted variable rate was the biggest widely advertised discount ever by a Big Six Canadian bank.

TD's discounted rate on Tuesday brings its variable mortgage rate offer in line with BMO's.

TD spokeswoman Julie Bellissimo says its special five-year variable rate applies to new and renewed mortgages, as well as the variable rate term portion of certain TD home equity lines of credit.

"We are confident this is a strong offer for new and renewing customers, while ensuring we remain competitive in a changing environment," Bellissimo said in an emailed statement.

The moves come amid slowing mortgage growth. The Canadian Real Estate Association said Tuesday that national home sales volume sank to the lowest level in more than five years in April, falling by 13.9 per cent from the same month last year. The national average sale price decreased by 11.3 per cent year-over-year.

Home sales have slowed due to various factors, including measures introduced the Ontario and B.C. governments to cool the housing market, such as taxes on non-resident buyers.

Other headwinds for mortgage growth include higher interest rates and a new financial stress test that makes it more difficult for would-be homebuyers to qualify with federally regulated lenders, such as the banks.

As of Jan. 1, buyers who don't need mortgage insurance must prove they can make payments at a qualifying rate of the greater of two percentage points higher than the contractual mortgage rate or the central bank's five-year benchmark rate. An existing stress test also stipulates that homebuyers with less than a 20 per cent down payment seeking an insured mortgage must qualify at the central bank's benchmark five-year mortgage rate.

The tighter lending rules are making it harder for homebuyers to qualify for uninsured mortgages, and shrinking the pool of qualified buyers for higher-priced homes, CREA's chief economist Gregory Klump said in April.

Meanwhile, Canada's largest lenders all raised their benchmark posted five-year fixed mortgage rates in recent weeks as government bond yields increased, signalling a rise in borrowing costs.

In turn, the central bank's five year benchmark qualifying rate -- which is calculated using the posted rates at the Big Six banks -- increased last week to 5.34 per cent. This qualifying rate is used in stress tests for both insured and uninsured mortgages, and an increase means that the bar is now even higher for borrowers to qualify.

National home sales sink 14% to lowest level in 5 years: CREA

TORONTO -- The Canadian Real Estate Association said national home

sales sank 13.9 per cent year-over-year to the lowest level in more than

five years in April, just as the number of newly-listed homes fell to a

nine-year low for the month.

The decreases amount to a 2.9 per cent drop in sales between March and April, bringing the total to 36,297. During that same time listings fell to 67,616, taking a 4.8 per cent hit -- a sign that the flurry of activity that usually kicks off the spring real estate market has failed to materialize.

CREA attributed the subdued level of activity to the stricter regulations for uninsured mortgages that the Office of the Superintendent of Financial Institutions introduced on Jan. 1. Its president Barb Sukkau said the regulations have "cast its shadow over sales activity," while its chief economist blamed them for having "destabilized market balance for housing markets in Alberta, Saskatchewan and Newfoundland."

CREA said 60 per cent of all local markets were balanced in April, but that sales were down in 60 per cent of all markets, led by the Fraser Valley, Calgary, Ottawa and Montreal.

Similarly, activity was below year-ago levels in about 60 per cent of all markets, which was "overwhelmingly" led by B.C.'s lower mainland and markets in and around Ontario's Greater Golden Horseshoe region.

CREA also said the country has experienced a decrease in the non-seasonally adjusted national average sale price, which dropped by 11.3 per cent year-over-year last month to just over $495,000.

That number is well below the April averages for markets in B.C. and Ontario that overheated last year, causing both provinces to spring into action to cool the sector. B.C.'s most recent budget introduced a speculation tax targeting both foreign and domestic buyers not paying tax in the province. Last April, the Ontario government aimed to quell its roaring markets with expanded rent controls, a plan to ensure property tax parity for new apartment buildings and legislation that would allow Toronto and other municipalities to implement a vacant homes tax.

Following those measures, CREA said April's non-seasonally adjusted average home price in Greater Vancouver was just above $1 million, in Toronto it was $804,584, in the Fraser Valley it was $780,736 and in Victoria it hit $703,592.

Those numbers were much higher than those experienced in Newfoundland and Labrador, Saint John, Sherbrooke, Saguenay, Quebec, Gatineau and Windsor-Essex markets, where the average home price in April hovered between $200,000 and $300,000.

The decreases amount to a 2.9 per cent drop in sales between March and April, bringing the total to 36,297. During that same time listings fell to 67,616, taking a 4.8 per cent hit -- a sign that the flurry of activity that usually kicks off the spring real estate market has failed to materialize.

CREA attributed the subdued level of activity to the stricter regulations for uninsured mortgages that the Office of the Superintendent of Financial Institutions introduced on Jan. 1. Its president Barb Sukkau said the regulations have "cast its shadow over sales activity," while its chief economist blamed them for having "destabilized market balance for housing markets in Alberta, Saskatchewan and Newfoundland."

CREA said 60 per cent of all local markets were balanced in April, but that sales were down in 60 per cent of all markets, led by the Fraser Valley, Calgary, Ottawa and Montreal.

Similarly, activity was below year-ago levels in about 60 per cent of all markets, which was "overwhelmingly" led by B.C.'s lower mainland and markets in and around Ontario's Greater Golden Horseshoe region.

CREA also said the country has experienced a decrease in the non-seasonally adjusted national average sale price, which dropped by 11.3 per cent year-over-year last month to just over $495,000.

That number is well below the April averages for markets in B.C. and Ontario that overheated last year, causing both provinces to spring into action to cool the sector. B.C.'s most recent budget introduced a speculation tax targeting both foreign and domestic buyers not paying tax in the province. Last April, the Ontario government aimed to quell its roaring markets with expanded rent controls, a plan to ensure property tax parity for new apartment buildings and legislation that would allow Toronto and other municipalities to implement a vacant homes tax.

Following those measures, CREA said April's non-seasonally adjusted average home price in Greater Vancouver was just above $1 million, in Toronto it was $804,584, in the Fraser Valley it was $780,736 and in Victoria it hit $703,592.

Those numbers were much higher than those experienced in Newfoundland and Labrador, Saint John, Sherbrooke, Saguenay, Quebec, Gatineau and Windsor-Essex markets, where the average home price in April hovered between $200,000 and $300,000.

Friday, May 11, 2018

All About Mother's Day

Your wonderful, sweet mother is worth…no less than $68,875 per year, according to Insure.com’s annual survey quantifying the value of all of those labors of love she performs day in and day out.

If

you’re as insulted as I am, then let’s calm down together a bit. Though

I believe a mother’s value is beyond calculation, it’s clear that the

insurance information and tools site each year computes a Mother’s Day

Index for two reasons:

One

is to acknowledge that whatever kind of paid work they may do, mothers

get no day off from cooking, driving, helping with homework, taking care

of the kids and sundry other activities that Insure.com

includes in its Index, which rose 1.9% over last year’s value, meaning

she would actually be shortchanged for these efforts, if paid, given

today’s 2.1% inflation rate.

Its

second reason, doubtless, is to sell insurance. While that is

self-interested, I find it more praiseworthy than the first. It is an

important protection for the whole family! If Mom’s income would be

reduced following Dad’s untimely demise, life insurance is a moral and

financial imperative. Similarly, in the event of an unexpected death, a

life insurance policy would pay for services that must carry on and

which grandparents may be unwilling or incapable of performing on a

daily basis.

This matter is no exaggeration. Many Moms do go uninsured. I quote from Insure.com’s release:

…36 percent of women in an annual poll by Insure.com reported that they cannot afford a life insurance policy. But with the value of moms reaching nearly $69,000 a year, most families cannot afford to be without one.”

The news release continues:

Of the women who reported having either a term, whole or both types of life insurance policies, nearly a quarter reported paying $251-$500 annually for their policy – that’s less than $1.50 a day.”

It

bears mentioning that the cost of term life insurance for a young

person can be had quite cheaply – at less, even much less, than a dollar

a day.

But

beyond insurance, important though it be, I think there are a few

financially connected sort of lessons we can learn, even if your Mom,

like mine, is not a money person.

The

most basic is that whatever your issue is – not saving enough, can’t

control spending – you can actually achieve your goal if stop, consider

and emulate the countless and indefatigable sacrifices your mother has

made for you.

The

second is an awareness of longevity. In the normal course of life, a

mother predeceases her children. Factual as this is, it is nearly

impossible to wrap your head around it, meaning if the opportunity still

exists, you can still ask more questions, learn more, listen more and

express your gratitude.

The

third goes beyond investing and is reflected in how a mother views her

“portfolio.” If you have three investments, and two have displayed

handsome returns and one has not, you can say – “that’s great, I’m up.” A

mother finds no solace in two kids doing great and one experiencing

difficulty. Her heart beats for her children, no matter what, no matter

when. And it is this fact that gives lie to the very concept of Mother’s

Day, which is actually every day.

Culled from seekingalpha.com

Subscribe to:

Comments (Atom)